AI

Written with AI assistance•23. April 2026•

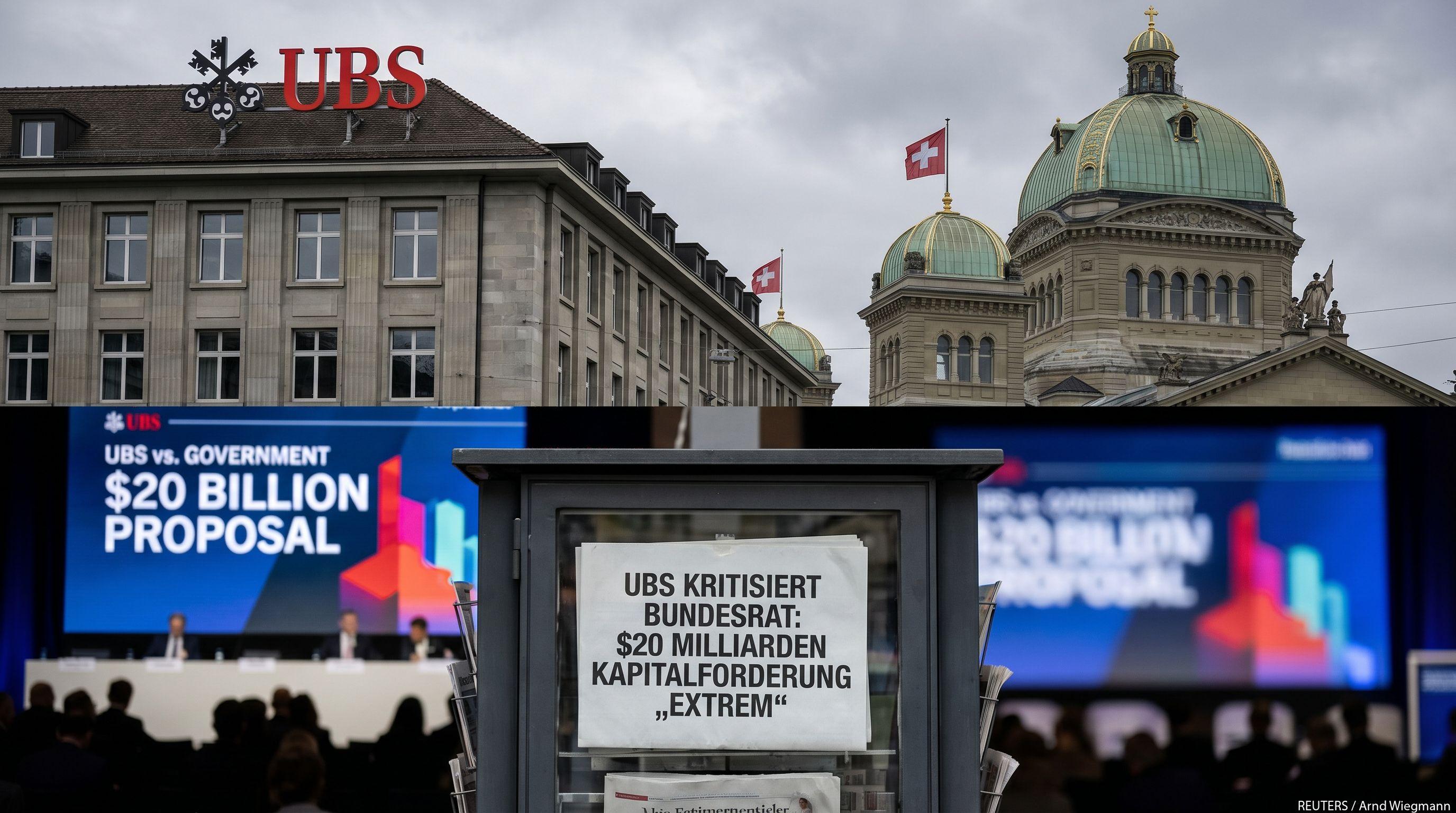

UBS has strongly rejected the Swiss government's proposal for increased capital requirements, labeling the measures 'extreme'. This sets the stage for a major political and financial battle over how to regulate the country's only 'too-big-to-fail' bank.

"The measures would have considerable consequences for the Swiss economy."

"Extreme."

A staggering $20 billion gap now stands between UBS and the Swiss government as a high-stakes regulatory war erupts in the heart of Europe’s financial capital. The Federal Council has officially approved a tightening of the screws that targets the nation’s only 'too-big-to-fail' institution with surgical precision. This is not merely a policy adjustment; it is a fundamental restructuring of the Swiss banking landscape designed to ensure that taxpayers never again foot the bill for a private banking collapse. The government's move comes as a direct response to the vulnerabilities exposed by recent market volatility, signaling that the era of lenient capital buffers is over. By demanding this massive capital injection, Bern is effectively putting UBS on a leash, prioritizing national economic security over the bank's immediate profit margins. The air in Zurich’s Paradeplatz is thick with tension as the financial titan grapples with a mandate that could redefine its global competitiveness.

A 100% coverage mandate for foreign subsidiaries is the explosive core of the new legislative draft. Currently, UBS and other systemically important entities are permitted to back their international holdings with approximately 50% debt financing. The government’s new proposal obliterates this practice, requiring every cent of book value in foreign branches to be backed by hard core equity capital held by the parent company. This shift confronts the 'double leverage' risks that have long haunted international regulators. By forcing UBS to fully collateralize its global footprint with Tier 1 capital, the Swiss government aims to insulate the domestic economy from shocks originating in New York, London, or Hong Kong. While the transition is slated for a seven-year phase-in period, the immediate implications for the bank's capital allocation strategy are profound. UBS must now choose between shrinking its international presence or diluting shareholder value to meet these stringent new benchmarks.

UBS has slammed the government’s proposal as 'extreme,' launching a fierce counter-offensive against what it describes as misleading regulatory statements. In a bold position paper, the bank warned that these measures would have 'considerable consequences' for the broader Swiss economy, potentially stifling credit and reducing Switzerland's attractiveness as a global financial hub. The bank’s leadership is not just resisting the $20 billion figure; they are challenging the very logic of the Federal Council’s assessment. UBS contends that the proposed package fails to account for the bank's existing stability and the unique complexities of its post-merger structure. This rejection sets the stage for a dramatic showdown next Wednesday, when the bank is expected to use its first-quarter results presentation as a platform to further dismantle the government's case. The rhetoric is escalating rapidly, with UBS framing the capital hike as a threat to the nation's prosperity, while the government frames it as the only way to save it.

The theater of conflict now shifts to the Swiss Parliament, where a summer session debate will determine the future of the nation's financial sovereignty. Lawmakers face an unprecedented dilemma: support the Federal Council’s aggressive safety net or side with a banking sector that remains a cornerstone of the Swiss identity. The outcome of this debate will resonate far beyond the borders of the Alpine nation, serving as a litmus test for global 'too-big-to-fail' regulations. If Parliament adopts the text without significant dilution, it will signal a permanent shift toward a more interventionist Swiss state. Conversely, a victory for UBS in the legislative chambers would maintain the status quo but leave the government vulnerable to accusations of complacency. As the seven-year implementation clock waits to be started, the world watches to see if Switzerland will prioritize the survival of its biggest bank or the protection of its taxpayers. The stakes could not be higher, and the battle for the soul of Swiss finance has only just begun.